Key points

– The key changes are a wind back in negative gearing, the taxation of real capital gains, numerous moves to reduce regulation, and modest net budget cuts over five years.

– The projected deficits are now slightly lower over the budget period by around $45bn, mainly due to more windfall revenue.

– With more stimulus in the near term though the Budget does nothing to make the RBA’s job in controlling inflation easier.

– The Budget continues to lock in structurally higher spending and budget deficits for the medium term.

– The tax changes look more like tax hikes than real tax reform and there is more work to do to boost productivity.

Introduction

This Budget is the most consequential in years given the Government’s committing to address poor productivity – and by implication stagnant living standards – while also dealing with the impact of the global oil shock and issues around intergenerational equity. As such it’s seeking to improve fairness, productivity and fiscal responsibility.

Key budget measures

Many of the key measures were pre-announced or leaked, but include:

- Negative gearing for new buys from now on restricted to new homes from 2027-28 onwards. For established homes losses can be used to offset other property income and can be carried forward. Shares and commercial property exempt from the change.

- The 50% capital gains tax discount to be replaced by the taxation of real gains from 2027-28 for all assets (with a likely exception for tech and startups) purchased from now and to face a minimum tax rate of 30%. CGT on existing assets to be assessed using a proportionate mix of the old and new tax models based on holding years. CGT on new builds given a choice of the old and new models.

- A minimum tax on discretionary trust distributions of 30%.

- A phased reduction of the EV fringe benefit tax break.

- Implementation of election promises with a 1% cut to the bottom tax rate (saving $5.15/week) & the $1000 standard tax deduction.

- A $250 income tax offset for all salaried workers for 2027-28.

- $20,000 instant asset write off for small business made permanent.

- Tax loss carry back so small biz can offset losses against past profits.

- The R&D tax credit expanded.

- Numerous moves to cut red tape with the aim of cutting regulatory costs by $10bn a year.

- Incentives & deals with states for productivity enhancing reforms.

- $2bn over 4 years to provide critical housing related infrastructure and $500m to speed up environmental approvals.

- $14bn in increased defence spending, $3.8bn for Melb rail project.

- $10.7bn “off-budget” to boost fuel reserves to 50 days plus.

- Gross spending cuts of $64bn incl NDIS, inland rail & public service.

Economic assumptions

Reflecting the impact of RBA rate hikes and the oil supply shock the Government sees inflation peaking at 5% and has revised down its growth forecasts for next year to 1.75% (from 2.25%) which is above the RBA’s forecast and implicitly assumes a smaller and short hit to growth from higher oil prices. The unemployment rate is still expected to reach 4.5%, unchanged from prior forecasts. As flagged in March it has also revised up its near-term immigration forecasts due to less departures but still seems a slowing to 225,000 in forward years which will slow population growth to around 1.3% pa. The Government kept its medium-term iron ore assumption at $US60/tonne but pushed it out to March 2027. With iron ore above that, it’s still a source of revenue upside.

Economic assumptions

|

2024-25 |

2025-26 |

2026-27 |

2027-28 |

2028-29 |

2029-30 |

||

| Real GDP | Govt |

1.3 |

2.25 |

1.75 |

2.25 |

2.5 |

2.5 |

| % year | AMP |

|

2.4 |

1.8 |

2.3 |

2.5 |

2.5 |

| Inflation | Govt |

2.1 |

5.0 |

2.5 |

2.5 |

2.5 |

2.5 |

| % to June | AMP |

|

4.8 |

2.4 |

2.6 |

2.5 |

2.5 |

| Wages | Govt |

3.4 |

3.25 |

3.5 |

3.5 |

3.5 |

3.75 |

| % to June | AMP |

|

3.1 |

3.3 |

3.2 |

3.5 |

3.5 |

| Unemp Rate | Govt |

4.2 |

4.25 |

4.5 |

4.5 |

4.5 |

4.25 |

| % June | AMP |

|

4.4 |

4.5 |

4.7 |

4.5 |

4.5 |

| Net migration | Govt |

305,000 |

295,000 |

245,000 |

225,000 |

225,000 |

225,000 |

Source: Australian Treasury, AMP

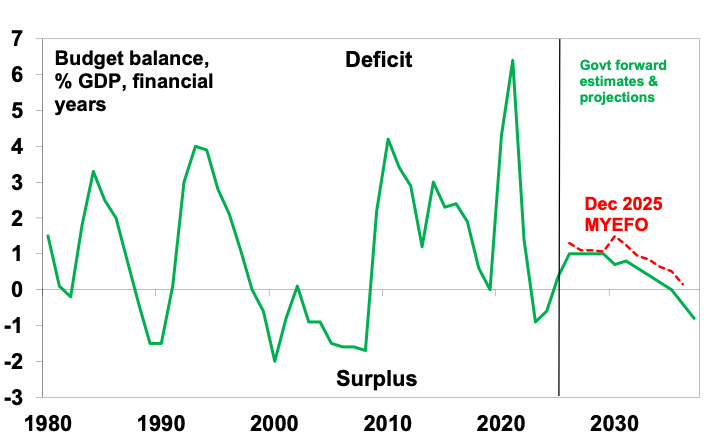

Still looking at big budget deficits

The Government is continuing to benefit from a windfall due largely to higher commodity prices (and hence resources profits) than assumed resulting in higher revenue. This is more due to good luck rather than good management. Compared to the projections in the December MYEFO this windfall – called “parameter changes” in the next table – is reducing the deficit over the five years to 2029-30 by another $37bn. This table – nicknamed the “table of truth” – also shows how much of the windfall has been spent or saved (see the “new stimulus” line). The good news is that in this Budget all the windfall is being saved and then some, with the government saving more than it spends to the tune of $8bn over the period to 2030. But all of the “savings” are in the later years, with near-term years still showing more new stimulus than previously expected.

The ”table of truth” – underlying cash budget balance projections

| 2025-26 | 2026-27 | 2027-28 | 2028-29 | 2029-30 | Total | |

| 25-26 Budget,$bn | -42.2 | -35.4 | -37.1 | -37.0 | ||

| Dec MYEFO, $bn | -36.8 | -34.3 | -36.2 | -36.0 | -52.1 | -195.4 |

| Parameter chg, $bn | +13.8 | +9.3 | +7.5 | -1.5 | +7.6 | +36.6 |

| New stimulus, $bn | -5.3 | -6.5 | -2.3 | +3.1 | +19.3 | +8.2 |

| 26-27 Budget,$bn | -28.3 | -31.5 | -31.0 | -34.4 | -25.2 | -150.6 |

| % GDP | -1.0 | -1.0 | -1.0 | -1.0 | -0.7 |

Source: Australian Treasury, AMP

This in turn means that thanks to the good luck of the revenue windfalls and net policy tightening for later this decade the budget is now projected to be in better shape than previously expected with a surplus by 2036.

Australian Federal budget deficit

Source: Australian Treasury, AMP

Gross public debt of nearly $1trn or 33% of GDP is projected to reach $1.2trn or 36% of GDP in 2028-29 before trending down.

Winners and losers

Winners include: wage earners, new and small businesses, first home buyers, venture capitalists, defence industry, and illegal tobacco users.

Losers include: new property investors in existing homes, older investors with limited income, high growth investors, beneficiaries of discretionary trusts, NDIS rorters and some new electric vehicle users.

Assessment

This Budget represents a good move in the right direction:

- It’s the first budget under the current Government to see all the revenue windfall saved and net budget savings over the forward estimates. So in this sense it’s more responsible than the last few budgets.

- It’s a significant package of moves to deregulate and encourage more business investment which should help boost productivity.

- There are more measures to help boost housing supply.

- It includes tentative moves towards tax reform in regards to the tax concessions – which may go some way to reduce perceptions of unfair advantage by older generations when it comes to housing.

- There is more scope for upside revenue surprise with still cautious commodity price assumptions.

And the budget deficit and debt ratios are a fraction of the averages for comparable countries, with the debt/GDP ratio being around half.

However, the Budget has several significant weaknesses.

- Structural deficits. While the budget deficits are now smaller than projected, they continue out to mid next decade despite another round of revenue windfalls and new tax measures. This sees no money put aside for a rainy day over the forecast period until 2036 which is off in the never never. The ratcheting up of spending on temporary revenue windfalls in past budgets leaves the budget vulnerable to a reversal of the windfalls.

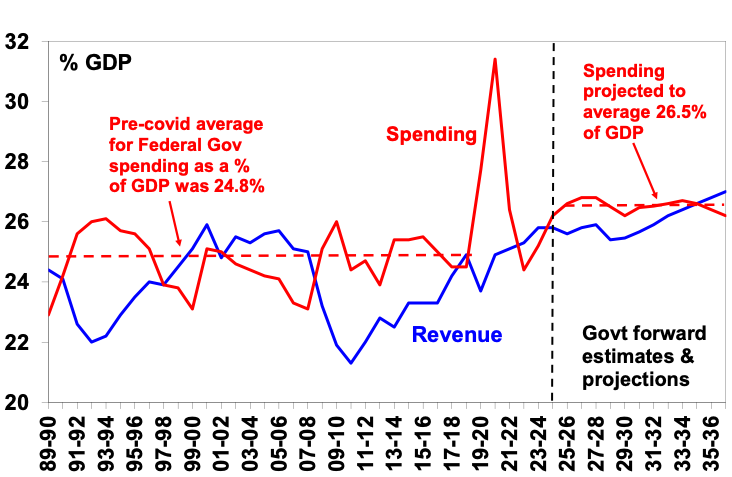

- Government spending was cut by far less than hoped leaving it higher than normal using up capacity in the economy. In the next two financial years net policy decisions have led to policy easing due to more spending. This arguably adds slightly to inflationary pressures in the economy rather than reduces them. And over the forward years policy has only tightened by $8.2bn due to increased revenue presumably flowing from the changes to tax concessions. And at a high level, Federal Government spending as a share of GDP over the next decade has been shaved only slightly to 26.5% from 26.9% in the December MYEFO this is still well above the pre-Covid average of 24.8%. This leaves little room for a pickup in private spending in the economy without hitting capacity constraints and higher inflation. And this is probably about as good as it will get as by next year’s budget we will bumping up against the next election where the pressure will be once again to ramp up spending.

Federal Government spending and revenue

Source: Australian Treasury, AMP

- Reliance on bracket creep and higher taxes to return to budget balance. Revenue is projected to start trending up from 2028-29 reaching a record 27% of GDP by 2036-37 as bracket creep kicks in. The rising burden on Millennials & Gen Z is unfair and unrealistic. Politicians will eventually want to give some back as “tax cuts”. But then how will we get back to surplus then?

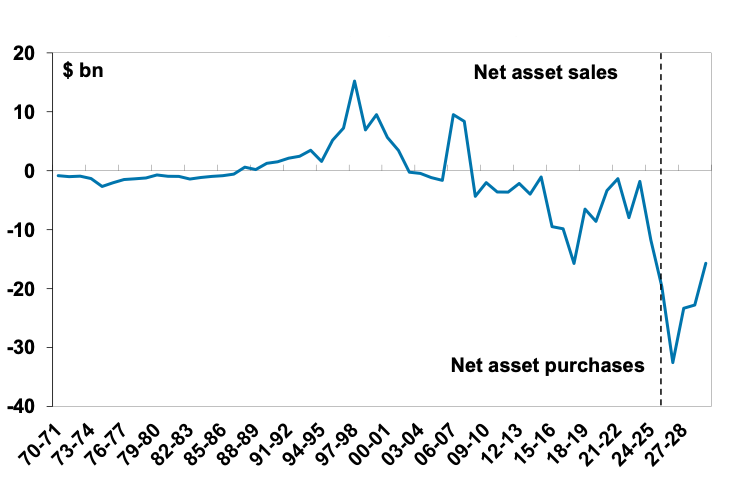

- Off budget spending. This remains a big issue as governments have been allocating increasing spending as “off-Budget” on the grounds that it’s an “investment”. This is resulting in a widening gap between the underlying cash balance (referred to above) and the headline balance (which includes “investments”). In fact, for the next financial year the headline deficit is projected to be $64.1bn compared to the underlying cash deficit of $31bn. However, much of this spending is not wise investment but it adds to public debt.

Headline minus underlying cash budget balance

Source: Australian Treasury, AMP

- Tax hikes are not tax reform. While curtailing access to tax concessions is a move in the direction of tax reform (as the CGT discount was arguably too generous and some rorted negative gearing) without addressing other failures in the tax system they amount to little more than a tax hike and are not tax reform. They have done nothing to ease Australia’s high reliance on income tax and will further add to the already very progressive nature of the Australian tax system – where the top 5% of taxpayers pay 32% of income tax collected and the top 10% pay nearly 50% – which will act as a further disincentive to work effort. Tax reform should be aimed at improving the tax system’s efficiency – so it distorts economic decisions and resource allocation less – by relying less on income tax and more on the GST. While income earned from assets may be taxed lightly relative to income earned as a wage and salary earner this should be addressed by lowering the taxation of income where our income tax rates are quite onerous compared to similar countries. Eg, the top marginal tax rate is well above the median of comparable countries and kicks in at a relatively low multiple of average earnings.

- More needs to be done to confidently boost productivity growth. To boost productivity growth – which is essential if we want to see faster growth in per capita GDP and hence living standards – the key things we need to see are: a reduction in the size of the public sector in the economy to free up resources for the more efficient private sector; tax reform to make the tax system simpler (so easier to comply with) and more efficient (so it distorts economic decisions less); and a range of reforms to make it easier for the private sector to grow and employ. The Budget saw some improvement but its modest overall: the public sector is still projected to remain larger than pre-Covid; the curtailment of the tax concessions may have boosted perceptions of fairness and improved simplicity but have done nothing to reduce the distortion to work incentive caused by our high reliance on income tax; and the moves to reduce regulation and encourage investment will help but there has been no move to address excessive labour market regulation. And “Future Made in Australia” subsidies run the risk of reducing productivity over time. So, all up there is likely a lot more to be done to confidently get sustainable productivity growth back to around 1.5% growth per annum.

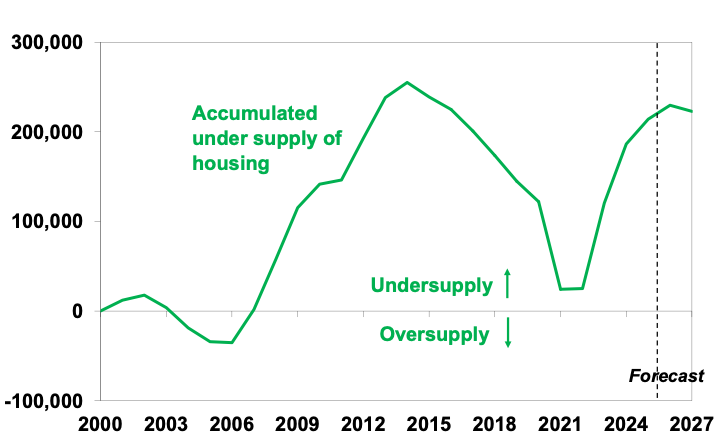

- Housing. The changes to negative gearings and the CGT discount could result in a 5% of so fall in home prices in the short term as investors retreat due to a fall in the perceived after-tax return to property investment and this will no doubt be chalked up as a win for the policy change. But it’s doubtful that the moves will boost housing affordability much over the longer term – as the basic driver of this is a shortage of housing relative to underlying population driven housing demand. While negative gearing is to remain for new homes it’s likely to result in unintended consequences by eg making it harder for first home buyers to get into new housing. And policies that reduce investor interest in property overall will likely lead to less housing supply not more – with even the Budget papers estimating that the tax changes will reduce supply by 35,000 homes over a decade. Rather the focus should be on addressing the fundamental housing demand-supply imbalance, but the Budget is now projecting slightly higher immigration and so more demand and it’s not clear that it will improve supply despite the $2bn for new housing infrastructure and given the hit from the tax changes. The Government was right in its first term to focus on boosting supply but now two years into the Housing Accord goal to produce 240,000 homes a year we have been running around 60,000 below target and so making no inroads into the undersupply of housing which we estimate to be between 200,000 to 300,000 dwellings.

The accumulated shortfall of housing in Australia

Source: ABS, AMP

- Fairness. The move to wind back housing tax concessions may be popular with younger voters but its more about optics than fundamentals. Older generations have got the benefit of these tax concessions to grow their wealth and now they are being curtailed for the young! What’s more as noted above the property tax changes are unlikely to fix the undersupply of housing. The key ways to improve intergenerational equity are to: boost productivity growth so living standards grow at a rate older generations experienced; get the housing balance right with more supply and less immigration; and raise the GST so as to raise more tax from older self-funded retirees – and yes that will include one of us in a few years’ time! – and cut income tax in order to lower the tax burden on workers. And as already noted the tax hikes may also be judged unfair for older higher income workers because they amount to a tax hike at a time when the income tax system is already highly progressive.

Implications for the RBA

While the new $250 Working Australia Tax Offset is trivial and doesn’t kick in until 2027-28, the near-term fiscal easing shown in the “table of truth” above (ie $6.5bn over the year ahead) won’t make the RBA’s job any easier. Nor will the handouts already announced in various state budgets. That said, it’s not enough to change our base case for just one more RBA hike in August. However, with poor household and consumer confidence levels and the Budget unlikely to add much to economic growth in the near term along with the ongoing blockage of oil through the Strait of Hormuz risking a recession we remain of the view that the RBA will be cutting rates next year.

Implications for investors – negative gearing & CGT

The changes to negative gearing, the CGT discount and the minimum tax on trust distributions have potentially big implications for many investors. I will leave the details to those with more expertise regarding taxation, but the changes to negative gearing are probably the most significant with about 1.2 million taxpayers reporting a loss for tax purposes on property. However, whether the CGT discount change is significant going forward will depend on the interaction of the rate of property price growth and inflation. Since the introduction of the discount in 2000 it has been beneficial to most investors as asset price gains were high and inflation was low. But if we go back into a period where property price growth is more constrained (say 5% pa) and inflation higher (at say 3% pa) then under scenarios where the holding period is 12 years or less investors may actually end up better off.

Where the CGT tax change may bite is in relation to shares and businesses – particularly those which don’t meet any carve out for startups. The removal of the 50% discount could take the CGT rate for a high-income earner from the low end of comparable countries to the high end. This in turn could work against growth shares and small businesses and attracting talented workers to such businesses which could work against the Budget’s objective to boost productivity.

Implications for Australian assets

Cash and term deposits – no major implications.

Bonds – the projection for smaller medium term budget deficits imply slightly less upwards pressure on bond yields.

Property – the curtailment of negative gearing and the CGT discount by making property less attractive to investors could knock around 5% off property prices in the short term as investors retreat due to lower after tax returns. This is likely to be compounded by the backdrop of RBA rate hikes. However, the dip is likely to prove temporary as the supply imbalance reasserts itself.

Shares – since shares (and all assets apart from property) are not affected by the changes to negative gearing they will benefit as an investment destination relative to property. The CGT change will boost the appeal of high dividend stocks over growth stocks. Super will also benefit as an investment destination versus property as it tax rules are unchanged.

The $A – the Budget is unlikely to change the rising trend for the $A.

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Diana Mousina – Deputy Chief Economist, AMP

My Bui – Economist, AMP

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.