Higher yields and income keep bonds resilient amid volatility

The first quarter of 2026 has delivered no shortage of headlines, with sharp moves in energy prices, ongoing geopolitical uncertainty and shifting expectations around inflation and growth. Against that backdrop, bond market volatility has increased, but without the kind of breakdown seen in more challenging periods. Higher yields mean bonds are now delivering more income. While prices may fluctuate, income has regained its importance in fixed income returns.

Volatility, not dysfunction

Higher oil prices have influenced near‑term inflation expectations and led to differing responses across global markets and a varied response from central banks. Yet despite the busy news cycle, bonds have largely behaved as expected.

This distinction matters. While volatility can create discomfort, it can also create opportunity, particularly for long term investors.

In this environment, market capitalisation weighted strategies, such as ETF’s can provide steady income and some return potential, while still offering support if growth slows.

The aim is to avoid leaning too far toward either short term positions or more interest rate sensitive long duration exposure while the outlook remains uncertain. As always, maturity positioning is most effective when aligned with the role fixed income is meant to play in the broader portfolio whether that is stability, income, diversification, or a combination of the three.

Inflation: short‑term shock versus longer‑term anchors

Inflation expectations have once again come into focus. Much of the recent discussion has been driven by higher energy prices and central banks have reinforced that inflation is a risk worth monitoring.

The market has largely treated the energy spike as a short-term shock, and longer-term inflation expectations have remained relatively anchored. This tension matters. While energy prices can lift inflation in the short run, if prices stay high for longer, the balance of risk may shift towards slowing growth. For investors the objective is to ensure portfolios are balanced to navigate a range of outcomes.

Avoiding reactionary decisions

One potential risk for portfolios during volatile periods is allowing short‑term headlines to drive long‑term decisions. We have seen some investors lean heavily toward cash, floating‑rate or very short‑duration strategies in response to uncertainty. While understandable, crowded positioning can limit future return potential once sentiment shifts.

Markets often move quickly on geopolitical developments, commodity prices or central bank commentary, but those moves do not always translate into lasting economic outcomes. A disciplined framework can help investors distinguish between temporary noise and information that genuinely alters the long‑term outlook.

A role for inflation‑linked bonds?

Inflation‑linked bonds are best viewed as tools for preparation rather than reaction. They are designed to provide protection when inflation risks are under‑appreciated by markets, rather than after inflation has become the dominant concern.

Inflation‑linked bonds can lag when growth slows, so traditional government bonds often provide better protection in those periods. For that reason inflation-linked bonds tend to work best as a complement within fixed income, sized to suit an investor’s goals and comfort with risk.

Income is doing the work

While quarterly returns for bonds have been modestly negative, income has behaved as expected. With higher yields, bonds are earning more of their return through regular income, which helps steady results over time. With much of the year still ahead, that income continues to provide support.

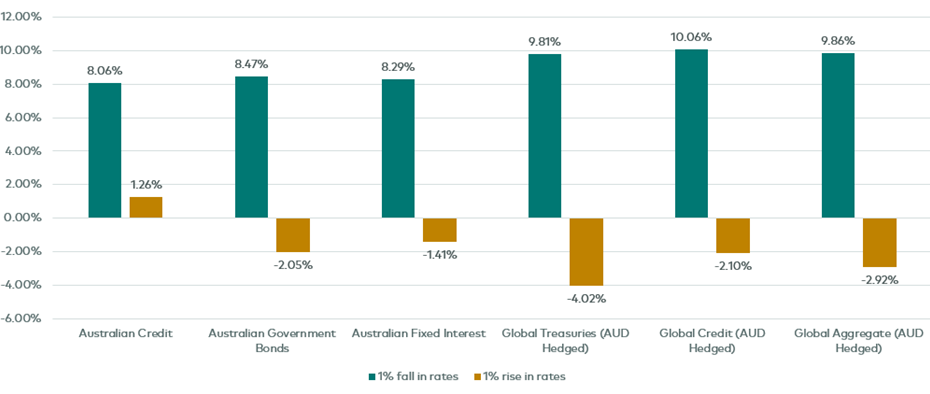

Impact of a 1% rise or fall in interest rates

12 month total return

Notes: Assumes an immediate +/- 100bps parallel shift in the yield curve and adds the running yield of the index to determine a hypothetical 12-month total return. Data is for illustrative purposes only and shows the interest rate sensitivity in a theoretical scenario. Source: Vanguard and Bloomberg: Bloomberg AusBond Credit 0+ Yr Index, Bloomberg AusBond Treasury 0+ Yr Index, Bloomberg AusBond Composite 0+ Yr Index, Bloomberg Global Treasury Scaled Index, Bloomberg Global Aggregate Corp/Gov-related TR Index, Bloomberg Global Aggregate Float Adjusted TR Index. Data run 2 April 2026.

Bonds still offer a favourable balance, with limited downside and the potential for stronger returns if rates fall — something long‑term investors may find appealing.

Credit fundamentals remain supportive

Credit markets have shown resilience. Credit spreads have edged wider but are still in line with history, and demand for yield remains supportive. With uncertainty driving more differences between issuers, careful credit selection matters more than ever.

Rising uncertainty is increasing dispersion and opportunity

Source: Vanguard and Bloomberg

Overall, fixed income continues to offer a blend of income, diversification and optionality. While the path may not be smooth quarter to quarter, the underlying case for bonds remains intact for investors focused on long‑term outcomes.

This article contains certain ‘forward looking’ statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

Source: Vanguard

This article has been reprinted with the permission of Vanguard Investments Australia Ltd. Copyright Smart Investing™

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966).

The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

We have not taken your or your clients’ objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice – Offer not to persons outside Australia

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2026 Vanguard Investments Australia Ltd. All rights reserved.